MENU

Visa Intelligent Commerce brings AI-agent payments into familiar card-network infrastructure. Its role is to help agents transact through tokenized credentials, user-defined controls, authentication signals, and merchant acceptance paths that already exist across card commerce.

That addresses one part of the problem: trust at checkout.

AI agent payments do not always look like checkout. An agent may request a paid API, unlock a dataset, call an MCP tool, trigger a model workflow, or coordinate with another agent. In those cases, merchants need more than card-network acceptance. They need to know what the agent used, which rule authorized the action, how usage should be priced, and how revenue should settle.

As the World Economic Forum notes in its AI Agents in Action report, agent adoption depends on enforceable authorization, auditability, and clear accountability. In payments, that means the stack has to support more than checkout. It needs scoped permission, usage records, access control, and settlement that can keep up with autonomous workflows.

Visa Intelligent Commerce applies when the core problem is allowing AI agents to transact through existing card-network rails. It brings structure to agent-led checkout by emphasizing tokenized credentials, user controls, authentication, and payment protection signals.

That makes it relevant for merchants, issuers, and platforms that want agent payments to stay close to familiar card acceptance. A user can authorize an agent, the agent can act within defined controls, and the transaction can move through established card infrastructure.

In those commerce use cases, card-network trust and merchant acceptance are central. A shopper may ask an agent to find an item, compare options, and complete a purchase.

The gap appears when the product is not a cart-based purchase.

AI services often monetize usage, not orders. An agent may consume a paid API ten times, trigger a tool action, unlock a data source, or request another agent’s service. Those workflows need usage records, pricing rules, access decisions, and settlement logic beyond the card transaction itself.

The relevant alternative depends on which part of the agent payment workflow a team needs to support.

Card-network tools apply when the main requirement is agent-led checkout through familiar payment rails. Checkout and commerce platforms apply when merchants want AI shopping experiences connected to existing payment operations. Wallet and identity tools support workflows where agents need to prove who they represent or access payment credentials. Banking tools apply when agents need to trigger transfers or financial workflows, an area the BIS has also explored in its work on AI agents in payment systems.

For AI services, the requirement is usually broader. A paid API request, MCP tool call, dataset unlock, or agent-to-agent task needs more than payment authorization. The merchant also needs to meter usage, apply pricing, enforce access, and reconcile revenue.

Agent-native payment infrastructure is relevant when permission, payment, usage, and settlement need to work together without requiring builders to assemble each layer from separate systems.

Nevermined provides payment infrastructure for AI agents, AI services, API providers, MCP tool builders, and agent marketplaces. It gives agents bounded payment capability while giving merchants the tools to meter usage, enforce access, and settle revenue.

Where Visa Intelligent Commerce is centered on card-network trust and agent-led checkout, Nevermined is centered on agent-native monetization. It connects authorization, usage records, pricing, access control, and settlement in one workflow.

The platform supports a card delegation workflow that lets users authorize agents without exposing raw card credentials. Agents receive scoped payment capability, while users define spending limits, time windows, merchant restrictions, transaction count rules, and revocation conditions.

For merchants, the x402 Facilitator coordinates authorization, metering, and settlement for APIs, agents, MCP tools, datasets, and protected resources. This connects the payment event to the service event when the agent consumes a paid digital resource.

Nevermined applies to teams selling AI services, APIs, datasets, MCP tools, agent workflows, compute, media, subscriptions, and usage-based products.

It is relevant when:

Nevermined covers both sides of the agent payment problem. The agent can pay under defined limits. The merchant can monetize what the agent uses.

That combination matters because AI agent payments rarely stop at “approve card transaction.” A single workflow may include multiple API calls, tool actions, dataset requests, and service responses. Nevermined gives teams the infrastructure to track those events and connect them to revenue.

Valory cut deployment time of their payments and billing infrastructure for the Olas AI agent marketplace from 6 weeks to 6 hours using Nevermined, clawing back $1000s in engineering costs.

Mastercard Agent Pay is another card-network framework for agent-led transactions. It focuses on tokenization, transaction attribution, user-defined controls, and network-level governance for agent-led commerce.

The model keeps agent-led payment activity within existing card payment patterns while adding structure around transaction attribution and user-defined controls.

Mastercard Agent Pay applies to commerce teams, issuers, and platforms that need card-network compatibility for agent-led transactions.

Card-network governance can support payment trust and attribution. It does not automatically create merchant-side usage metering, pricing plans, access rules, or settlement records for AI services.

For APIs, datasets, MCP tools, and usage-based AI products, teams usually still need a layer that connects agent activity to revenue.

Stripe Agentic Commerce Suite brings agent-assisted purchasing into Stripe’s broader payment and checkout platform. It applies to merchants that already use Stripe and want products or checkout flows to appear in AI shopping environments.

This makes Stripe different from Visa in emphasis. Visa operates at the card-network layer. Stripe operates closer to merchant payment operations, checkout, billing, and platform workflows.

Stripe applies to merchants already using Stripe for payments, billing, subscriptions, marketplaces, or checkout who want to extend those flows into AI-assisted commerce.

Stripe remains oriented around checkout and payment processing workflows. Agent-native services may need more granular infrastructure around each service event.

A paid API request, MCP tool call, or dataset unlock needs metering, entitlements, access logic, and settlement tied to usage. Those layers may sit outside a standard checkout workflow.

PayPal Agentic Commerce focuses on AI-assisted shopping, product discovery, checkout, and order workflows. It is relevant for merchants that want to sell through AI shopping channels while using PayPal-supported payment and account infrastructure.

PayPal is not a direct card-network equivalent to Visa. It applies when the buyer relationship already includes PayPal, Venmo, or PayPal-supported checkout.

PayPal applies to merchants that want AI shopping experiences connected to familiar consumer payment accounts and order-management workflows.

Consumer checkout support does not cover the full agent monetization stack. Teams selling paid APIs, datasets, MCP tools, or agent services still need usage records, pricing logic, access rules, and settlement tied to what the agent consumed.

PayPal supports shopping and checkout transactions. AI service monetization needs a deeper connection between agent action and revenue.

Coinbase x402 is an HTTP-native payment protocol built around the 402 Payment Required status code. It lets a service return a machine-readable payment requirement when an agent, application, or user requests access to a protected resource.

This is different from Visa’s card-network approach. x402 is not mainly about card acceptance. It is about making payment requests part of the web interaction itself.

x402 applies to developers building paid APIs, paid tools, digital resources, and software-readable payment flows.

x402 can define how a service asks for payment, but it does not manage the full business workflow around monetization.

Teams still need customer plans, pricing rules, usage records, refund handling, access control, reporting, and compliance workflows around the protocol.

Crossmint provides agent wallet and commerce infrastructure. It is relevant when agents need wallets, smart accounts, virtual cards, or payment tools to transact across digital or merchant environments.

Compared with Visa Intelligent Commerce, Crossmint sits closer to the agent wallet and buyer-side payment layer. It provides infrastructure for agents to hold or use payment tools, while merchant-side monetization may still require another layer.

Crossmint applies to teams building agents that need wallet infrastructure, payment tools, virtual cards, smart accounts, or commerce access.

Wallet and card tools support agent spending workflows. They do not automatically tell a merchant how to price a service event, meter an API call, enforce access, or reconcile revenue.

For AI products, buyer-side payment capability and merchant-side monetization are related but separate problems.

Skyfire focuses on agent identity, user mandates, and payment capability. It helps answer whether an agent is legitimate, who it represents, and whether it has permission to act.

Skyfire applies when the core issue is trust at the point of interaction, including workflows where agents interact with existing websites, tools, or checkout flows.

Skyfire applies to teams prioritizing agent identity, payment mandates, checkout access, and trust signals for autonomous buyers.

Identity and mandate signals are not the same as monetization infrastructure. A merchant still needs to price usage, meter tool calls, enforce entitlements, and settle revenue when an agent consumes a paid service.

That is the distinction between knowing an agent is authorized and knowing how much the agent used.

Payman AI focuses on controlled banking and payment operations for agents. It is designed for workflows where agents need to initiate payments, transfer funds, analyze accounts, or complete financial tasks on existing rails.

This makes Payman different from Visa Intelligent Commerce. Visa is about card-network agent payments. Payman is closer to banking automation and finance operations.

Payman applies to teams building agents that need controlled payment actions, account analysis, transfers, or finance workflow automation.

Banking automation does not automatically translate into AI service monetization. A platform selling usage-based digital products still needs product-level pricing, access control, tool usage records, and settlement workflows tied to what the agent consumed.

Payman applies to finance workflows. AI commerce teams may still need a payment-to-usage layer for product-level monetization.

Nevermined fits payment workflows that need to connect authorization, usage, access, pricing, and settlement.

That includes:

Nevermined functions as the coordination layer between agent permission and merchant-side revenue operations. It can map a permitted agent action to a usage event, check whether access should continue, and route the transaction through the appropriate settlement path.

Protocol coverage supports that workflow without making the article repeat the same integration list. For example, per-request billing can apply to HTTP-based services, while direct integration can apply when agents access paid tools through MCP. The same payment layer can also support agent-to-agent workflows and standardized payment coordination as these patterns mature.

Nevermined is positioned for AI agent payment workflows that involve more than agent-led checkout. It combines delegated spending, usage metering, access control, protocol support, and settlement in one platform. Visa Intelligent Commerce focuses on card-network trust and tokenized agent transactions. Nevermined is broader for AI services because it helps agents pay while helping merchants monetize what agents consume.

Visa Intelligent Commerce works at the card-network and agent-trust layer. Nevermined works at the agent-native payment and monetization layer. It gives agents scoped payment capability and gives merchants infrastructure for usage records, access control, pricing, and settlement. This makes Nevermined applicable when the product is consumed repeatedly, such as paid APIs, tools, datasets, or usage-based AI services.

x402 is useful for machine-readable payment requests, especially when APIs or protected resources need to request payment over HTTP. However, x402 is a protocol rather than a complete payment and monetization platform. Teams still need usage metering, pricing plans, access control, customer management, and reporting. Nevermined builds around x402 by adding the operational layers needed for production agent commerce.

AI agent payment systems should support scoped payment authority, tokenized credentials, spend limits, revocation, audit trails, and usage records. Agents should receive only the capability needed for an approved task, not unrestricted access to a payment method. Nevermined supports this model through delegated spending, programmable guardrails, and payment-aware usage records. These controls help buyers and merchants manage risk as agents transact autonomously.

Yes. Agent payment infrastructure can support both card-based flows and stablecoin settlement when the platform coordinates authorization, metering, and settlement across multiple rails. Nevermined supports fiat rails, credits, smart accounts, and stablecoin settlement flows through one agent-native payment layer. This gives builders more flexibility when different agents, buyers, or merchants prefer different payment paths.

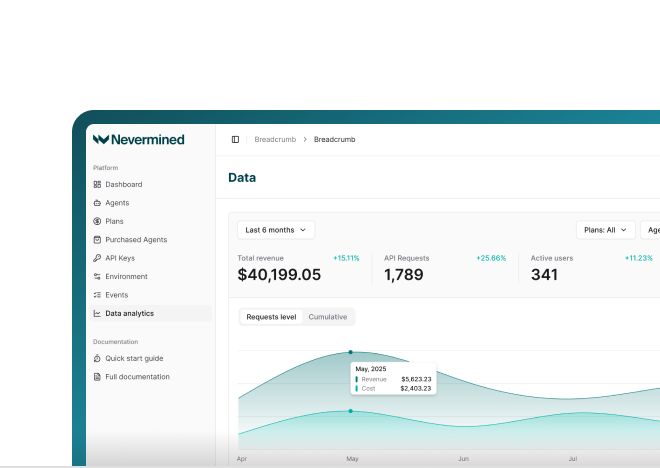

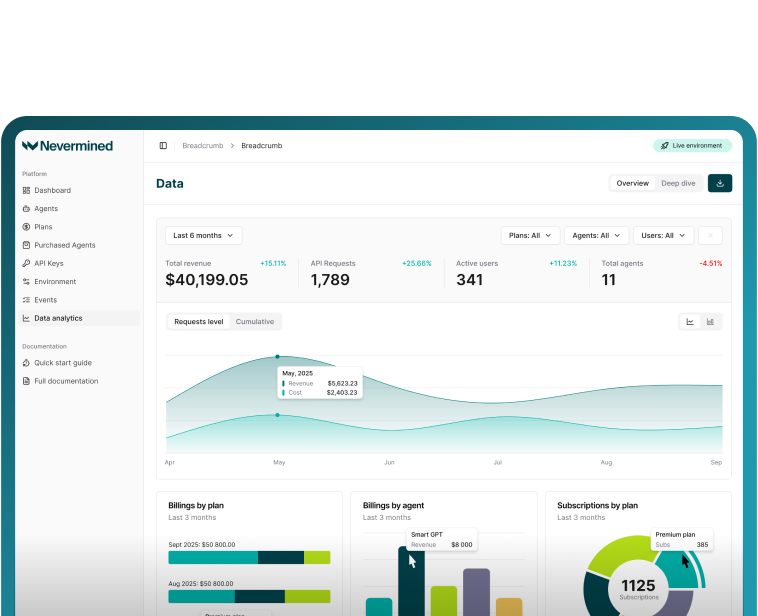

See Nevermined

in Action

Real-time payments, flexible pricing, and outcome-based monetization—all in one platform.