MENU

AI agents can use credit cards, but the infrastructure required differs fundamentally from traditional human payment systems. Two distinct paradigms exist: AI agents deployed by financial institutions to monitor transactions and detect fraud, and AI agents that autonomously make purchases using specialized virtual card infrastructure. The second paradigm represents a transformative shift where autonomous software becomes an economic participant, requiring new payment rails, security protocols, and compliance frameworks. For businesses building AI agents that need to transact autonomously, purpose-built payment infrastructure provides the metering, settlement, and compliance capabilities that traditional processors cannot deliver.

Traditional credit card payment systems were designed with a fundamental assumption: a human is present to authenticate, approve, and complete every transaction. This assumption breaks down entirely when AI agents need to operate autonomously, creating five critical risks that traditional payment infrastructure cannot address.

Giving AI agents unrestricted access to personal or corporate credit cards creates significant exposure. According to payment security analysis, the core risks include:

Technology experts consistently warn against providing AI agents with unrestricted credit card access. Matt Kropp, AI Expert at Boston Consulting Group, stated that agentic commerce is "pretty risky right now" because there are not enough guardrails in the system for people to feel comfortable with agents autonomously buying things.

A single agent interaction can trigger hundreds of API calls costing fractions of a cent each. Common online processing fees like 2.9% plus $0.30 per transaction make sub-dollar requests margin-negative. When agents execute $0.15 tasks, fixed fees consume the entire transaction value.

Real incidents demonstrate the magnitude of this problem. Users have reported recent increases in API costs including cases where $1 of spend dropped from roughly 100k UCR to just 8k UCR. These runaway costs occur because traditional payment systems lack the granular controls needed for autonomous agent operations.

Capgemini reports that trust in fully autonomous AI agents has declined sharply; one section says 22% of executives trust fully autonomous agents, down from 43% in 2024, while the executive summary also cites 27% organizational trust.

This decline occurs even as 79% of organizations report adopting AI agents and U.S. financial institutions deploy autonomous finance systems.

Andrew Lee, founder of Tasklet, captured this sentiment when he noted that agents are fundamentally hard to trust for shopping tasks. His company's agent once booked a $30,000 speaking slot at Davos that the user could not afford.

The limitations of traditional credit card systems have driven the emergence of agent-native payment protocols designed from the ground up for autonomous transactions.

Multiple payment protocols have emerged to address the unique requirements of AI agent commerce:

Andrew Shikiar, CEO of the FIDO Alliance, observed that preexisting payment models were not built to contemplate actions performed on a user's behalf. The industry stands at a similar precipice as it did with passwords decades ago.

Six competing standards currently vie for adoption: x402, AP2, MCP, A2A, TAP, and ACP. This fragmentation creates risk for builders implementing proprietary integrations that may become obsolete as the ecosystem converges.

A protocol-agnostic approach ensures compatibility as standards evolve. Native support for x402 and A2A protocols enables interoperability across the emerging agent economy without locking into any single standard.

The FIDO Alliance, with contributions from Google and Mastercard, launched working groups to develop industry standards for validating and protecting agent-initiated transactions. Cloudflare partnered with Visa and Mastercard on Web Bot Auth to cryptographically authenticate agent traffic and distinguish legitimate agents from malicious bots.

Stavan Parikh, VP and GM of Payments at Google, explained that AP2 aims to provide cryptographic proof that a transaction was authorized by the user while maintaining privacy through selective disclosure. Different players in the ecosystem only see the information relevant to them.

Purpose-built payment infrastructure for AI agents addresses the fundamental gaps that traditional credit card processors cannot bridge.

Real-time settlement eliminates the 1-3 business day delays that complicate margin tracking in traditional payment systems. Payment infrastructure designed for agents supports instant settlement in both fiat through integrations with payment processors and cryptocurrency through stablecoin settlement on networks like Polygon, Gnosis Chain, and Ethereum.

The x402 facilitator coordinates authorization, metering, and settlement across payment types, providing a unified payment handshake that works regardless of underlying payment rails.

Traditional credit card transactions support only per-transaction pricing. Agent-native infrastructure enables three distinct pricing models:

ERC-4337 smart accounts with session keys enable programmable authorization logic where users authorize payment policies once, then agents transact freely within boundaries. This contrasts with standard x402 implementations that require wallet pop-ups for each request.

The trust deficit around autonomous agent payments requires infrastructure that provides verifiable transparency at every step.

Every usage record must be cryptographically signed and pushed to an append-only log at creation, making it immutable. The exact pricing rule stamps onto each agent's usage credit, allowing developers, users, auditors, or agents to verify that usage totals match billed amounts per line-item.

This zero-trust reconciliation model addresses concerns about trusting AI agents to manage tasks autonomously. When disputes arise, observability infrastructure provides complete audit trails showing exactly what the agent requested, what it was charged, and how those charges map to pricing rules.

Virtual cards represent only 9% of fraudulent transactions, demonstrating the effectiveness of tokenized, single-use payment credentials. This security advantage applies directly to agent payments where each transaction can use unique cryptographic credentials.

Agentic tokens build on this foundation by embedding agent identification, spending guardrails, and cryptographic proof of user authorization directly into the token. Unlike traditional tokens that are indistinguishable from human transactions, agentic tokens make AI-initiated transactions visible and auditable to banks, merchants, and networks.

Compliance requirements for AI agent payments span multiple frameworks:

Audit-ready traceability through append-only logging satisfies regulatory review requirements. API and CSV export capabilities enable independent verification of metering data.

AI agents need persistent identities to participate in commerce, track reputation, and operate across different environments.

Each agent requires a unique wallet plus decentralized identifier (DID) with cryptographic proof of ownership. The ERC-8004 standard provides portable identities that work across environments, swarms, and marketplaces without re-wiring.

This identity layer enables:

When a user delegates $500 per week spending authority to an AI agent for three months, restricted to pre-approved SaaS merchants, the agent can autonomously purchase API credits, renew subscriptions, and provision cloud resources within those parameters.

The card delegation model enables this workflow. Users enroll their card once via a PCI-compliant vault, set spending mandates with amount caps, time windows, and merchant categories, then delegate a scoped API key to the agent. Card data never touches the payment platform; only secure network tokens are stored.

As agents collaborate and delegate tasks to other agents, attribution becomes critical for billing and accountability. Agent-to-agent monetization infrastructure tracks which agent requested which service and allocates costs accordingly.

Auto-discovery via Google's A2A protocol enables instant agent connection. Agents can find and engage services programmatically without human intervention, negotiating pricing and executing payments at machine speed.

Credit card transaction models force rigid per-transaction pricing that does not align with how agents consume and deliver value.

Most billing platforms support only usage-based models. Agent-native infrastructure supports three pricing approaches simultaneously:

Credits operate as prepaid consumption-based units redeemed directly against usage. This model provides several advantages over traditional credit card billing:

Credits align price to value by charging for micro-actions and rewarding successful outcomes. A publisher can price individual article access at $2 rather than requiring a $500 annual subscription, capturing revenue from traffic previously blocked by paywalls.

Dynamic pricing engines enable cost-plus-margin automation where platforms define exact margin percentages locked onto usage credits. This automation eliminates manual pricing updates when underlying costs change.

For example, when an LLM provider increases API pricing, the dynamic engine automatically adjusts downstream pricing to maintain configured margins. This protects builder economics without requiring manual intervention.

AI agents need infrastructure that coordinates complex payment flows across multiple settlement options.

A payment facilitator coordinates authorization, metering, and settlement across fiat, crypto, credits, and smart accounts. The x402 facilitator provides:

This coordination layer handles the complexity that would otherwise require custom engineering for every agent deployment.

Smart contract settlement on Polygon, Gnosis Chain, and Ethereum enables atomic "pay plus execute" transactions where payment and action occur as a single indivisible operation. This eliminates race conditions where agents execute actions without payment or pay without receiving service.

Additional smart contract capabilities include:

When multiple agents collaborate on a task, revenue must split across all contributors. A marketplace platform might take a percentage, the agent builder receives a share, and underlying service providers get their portion.

Traditional credit card processing cannot handle this complexity. Purpose-built infrastructure executes revenue splits automatically based on programmed rules, settling each party in their preferred currency without manual reconciliation.

The gap between needing agent payments and deploying them creates opportunity cost that compounds daily.

Building custom billing infrastructure for AI agents consumes engineering resources that could go toward product development. Nevermined gets you from zero to a working payment integration in 5 minutes, with SDKs for both TypeScript and Python.

Three-step integration covers most use cases:

Comprehensive technical documentation provides implementation guides, sandbox environments for testing, and API/CSV export for metering data verification.

The ecosystem supporting agent payments continues to expand. Development platforms like Buildship enable workflow-driven agent creation with built-in monetization. Marketplaces like Olas provide distribution for paid agents.

The AI agent market is projected to grow from $5.1B in 2024 to $47.1B by 2030. Financial services represents one of the highest-adoption verticals, driven by use cases spanning procurement, customer service, and operations automation.

Traditional card pricing often makes very small per-request payments uneconomic. Nevermined delivers the complete payment infrastructure stack for agentic commerce.

Nevermined Pay provides bank-grade enterprise-ready metering, compliance, and settlement so every model call turns into auditable revenue. Key capabilities include:

The platform provides native support for x402, Google's Agent-to-Agent (A2A) protocol, Model Context Protocol (MCP), and Agent Payments Protocol (AP2). This protocol-agnostic approach ensures compatibility as standards evolve, avoiding vendor lock-in that plagues proprietary systems.

For builders ready to add payments to their AI agents, Nevermined gets you from zero to a working payment integration in 5 minutes, with SDKs for both TypeScript and Python. The platform supports settlement on Polygon, Gnosis Chain, and Ethereum, with fiat integration through Stripe and stablecoin settlement through Coinbase.

Explore the documentation to start building, or review solutions for your specific use case.

Technically yes, but doing so creates significant risks. Sharing personal card numbers with agents provides no spend limits, no merchant restrictions, PCI DSS exposure, no audit trail, and full blast radius if compromised. Virtual cards with programmable controls or agentic tokens provide safer alternatives by scoping credentials to specific amounts, merchants, and time windows while maintaining audit trails.

Traditional processors were architected for human-present transactions with authentication at each step. They cannot economically handle micro-transactions where fixed fees exceed transaction value, lack the granular controls agents need for autonomous operation, and create billing blind spots through batch processing. Purpose-built infrastructure addresses these gaps with real-time metering, flexible pricing models, and instant settlement.

Usage-based pricing charges per token or API call, providing predictable unit economics. Outcome-based pricing charges for results like booked meetings or completed tasks, regardless of the computational resources required. Value-based pricing takes a percentage of ROI generated by agent actions, aligning builder and customer incentives. Agent-native infrastructure supports all three simultaneously.

Regular tokens (network tokens, device-bound tokens, gateway tokens) are indistinguishable from human transactions to banks and merchants. Agentic tokens represent a fourth type specifically designed for AI agents. They carry embedded agent identification, spending guardrails, and cryptographic proof of user authorization, making AI-initiated transactions visible and auditable to all parties for the first time.

Liability frameworks for agent-initiated transactions remain undefined, though American Express has announced protections for cardholders against charges related to AI agent error. The safest current approach treats agent transactions as merchant-initiated transactions under existing card-on-file rules. Tamper-proof metering with cryptographic verification provides audit trails for dispute resolution, documenting exactly what the agent was authorized to do versus what it actually did.

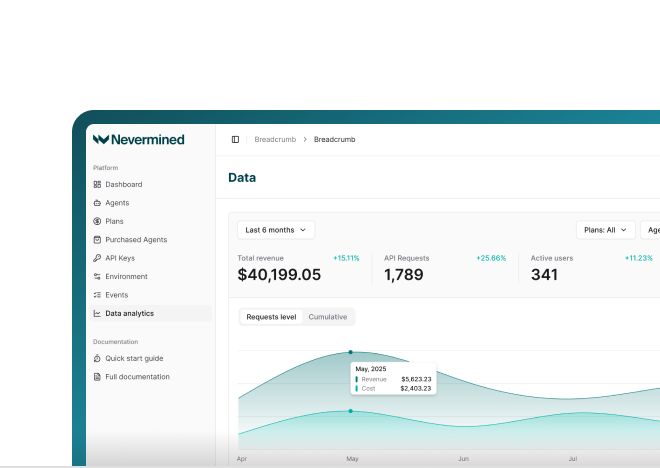

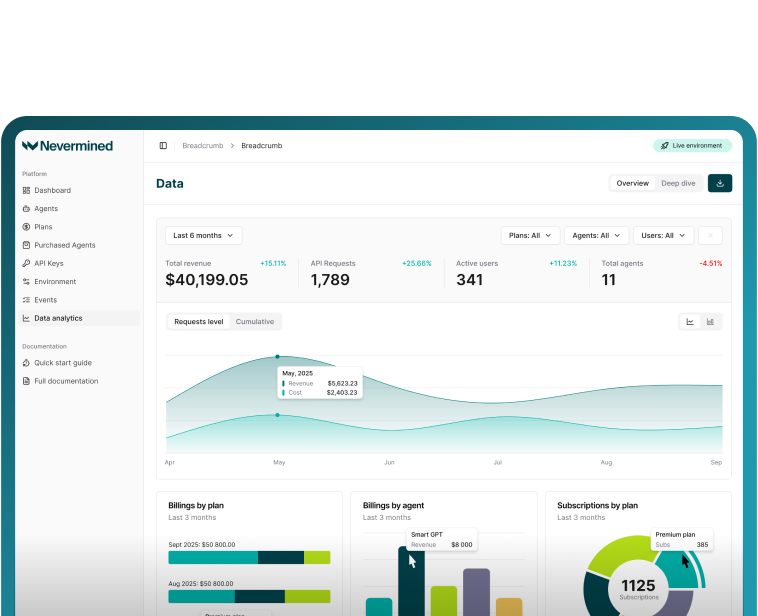

See Nevermined

in Action

Real-time payments, flexible pricing, and outcome-based monetization—all in one platform.