MENU

AI agents are beginning to buy access to APIs, tools, datasets, workflows, and digital services without a human completing every checkout step. McKinsey describes agentic commerce as a shift where AI agents can act on users’ behalf, navigate options, and execute transactions. That creates a new problem for merchants: traditional payment systems were designed around human approval, not autonomous software triggering payment requests inside service workflows.

For merchants, accepting autonomous payments requires more than payment acceptance. The system needs to verify agent authority, meter usage, enforce access, apply pricing, settle transactions, and keep audit-ready records.

A merchant needs to know whether an agent is allowed to pay before access is released. That includes who authorized the agent, what the agent can buy, how much it can spend, when the permission expires, and whether the payment request matches the allowed scope.

This matters because the “purchase” may not be a normal cart transaction. It may be an API call, MCP tool request, dataset unlock, compute task, protected file, or agent-to-agent service.

Autonomous payment flows often depend on what the agent actually does. A merchant may need to charge per request, per workflow, per tool execution, per dataset, per output, per subscription period, or through prepaid credits.

Metering connects service usage to pricing. Without it, a merchant may know that payment happened, but not what the agent consumed or how much revenue should be recognized.

In agent commerce, access should follow authorization. A protected resource should verify payment status, apply entitlements, release the service, and record the event.

This is especially important for APIs and MCP tools because the payment check may need to happen inside the request flow, not after a separate invoice cycle.

Merchants also need settlement records that finance, security, and compliance teams can review. Agent transactions should be traceable to the user mandate, agent identity, service event, pricing rule, and settlement method.

That is the difference between a simple checkout confirmation and an autonomous payment system built for production.

Nevermined gives merchants the infrastructure to charge AI agents for access to digital services. Instead of treating every transaction like a human checkout, Nevermined lets merchants connect payment verification directly to the service request.

That matters when the merchant sells something an agent consumes programmatically: an API response, MCP tool call, dataset query, workflow execution, protected file, or agent service. The merchant needs to know whether the agent is authorized to pay, whether access should be released, what usage occurred, and how revenue should settle.

The x402 Facilitator handles that merchant-side payment flow. It coordinates authorization, metering, access, pricing, and settlement across fiat rails, crypto rails, credits, and smart accounts. Nevermined also supports delegated card spending through its card delegation workflow, where agents receive scoped payment capability instead of raw card credentials.

Nevermined is relevant for merchants because it turns autonomous access requests into payable events. A service can require payment, verify authorization, meter the request, release access, and record settlement without forcing the agent into a human checkout flow.

That makes Nevermined a strong fit for merchants whose revenue depends on programmatic usage. Instead of only confirming that a payment happened, Nevermined helps merchants track what the agent consumed, which payment rule applied, whether the agent should keep access, and how the transaction should be reconciled.

Valory cut deployment time of its payments and billing infrastructure for the Olas AI agent marketplace from 6 weeks to 6 hours using Nevermined, clawing back $1000s in engineering costs.

x402 is an open payment protocol built around the HTTP 402 Payment Required status code. It lets a merchant or service request payment inside an HTTP interaction, allowing agents and software clients to respond programmatically.

For merchants, x402 is useful when the product is a paid API, MCP tool, dataset, protected resource, or digital service that agents need to access on demand. Instead of pushing every buyer through a checkout page, the service can return a machine-readable payment requirement.

x402 gives autonomous payment flows a shared request pattern. That makes it important for merchants that want agents to pay for individual API calls, tool executions, or protected resources without a human checkout step.

Stripe is a major payment infrastructure provider for online businesses, SaaS companies, marketplaces, and merchants. Its agentic commerce work gives merchants a path to connect AI-assisted shopping and payment experiences to existing payment operations.

For merchants already using Stripe, this can reduce adoption friction. Teams can keep familiar payment processing, billing, checkout, subscriptions, invoicing, marketplace payments, and financial operations while exploring AI-assisted purchase flows.

Stripe is relevant because many merchants already use it as their core payment and billing platform. For human-facing commerce and agent-assisted checkout, it gives teams a mature payment foundation.

Crossmint provides agentic payment infrastructure across wallets, virtual cards, stablecoin flows, and checkout-oriented payment products. It is relevant when agents need payment tools to buy from digital merchants or complete purchases programmatically.

For merchants, Crossmint is most useful when the payment flow involves agent wallets, cards, stablecoin infrastructure, or commerce APIs that let agents transact through existing payment environments.

Crossmint is relevant because agent commerce often needs buyer-side payment instruments. Wallets, cards, and stablecoin tools can help agents complete purchases or interact with digital merchants.

Coinbase is closely associated with crypto-native agent payments through AgentKit, wallets, Base ecosystem tooling, and x402-related developer infrastructure. This makes it relevant for merchants and developers building around stablecoins, onchain wallets, and machine-readable payment flows.

For merchants that want crypto-native payments or x402-style API monetization, Coinbase’s ecosystem can provide useful building blocks.

Coinbase is important because it helped bring x402 and crypto-native agent payments into broader developer use. Its ecosystem fits teams that want agents to transact through wallets, stablecoins, and onchain payment flows.

Skyfire focuses on agent identity, trust, mandates, and payment access. Its Know Your Agent model is designed to help services understand which agent is acting, who it represents, and whether the agent has permission to transact.

For merchants, that trust layer matters. Accepting payment from an autonomous agent requires more than knowing that a payment method exists. The merchant also needs signals around agent legitimacy, user authorization, and transaction scope.

Skyfire addresses a core merchant question: should this agent be trusted to transact? That makes it relevant when payment acceptance depends on agent verification, user mandates, and transaction authorization.

Visa Intelligent Commerce brings agent-led transactions into card-network infrastructure. It focuses on tokenized credentials, user-defined controls, authentication, payment protections, and agent commerce signals across existing card rails.

For merchants, Visa matters because it connects agent-led activity to broad card acceptance. An agent may need to pay using familiar card infrastructure while staying within user-defined spending rules.

Visa is relevant because card networks will play an important role in agent-led commerce. Merchants that already accept cards may benefit from agent payment models that work through familiar network rails.

Mastercard Agent Pay focuses on tokenization, registered-agent concepts, user-defined controls, and transaction attribution for agent-led commerce. Its approach gives card-network participants a framework for safer agent-initiated payments.

For merchants, Mastercard is relevant when agent payment acceptance needs to stay compatible with familiar card-network flows while adding more structure around agent identity and transaction authorization.

Mastercard belongs on the list because agent-led payments need card-network support, tokenization, and transaction attribution. Its work gives merchants and partners another path for agent payment acceptance through established card infrastructure.

PayPal is positioning for agentic commerce through merchant tools, developer resources, wallet-based checkout, and AI-assisted shopping flows. Its existing merchant and consumer network gives it relevance when agents interact with familiar online checkout environments.

For merchants already using PayPal or Braintree, agentic commerce tools may extend existing payment operations into AI-assisted buying experiences.

Typical use case: Consumer-facing merchants, marketplaces, and platforms that want PayPal, Venmo, card, wallet, or Braintree-powered checkout paths for AI-assisted commerce.

PayPal is relevant because many merchants and consumers already use its payment network. It can be useful when agent-assisted commerce still depends on familiar checkout, wallet, and account flows.

PayOS provides payment and billing infrastructure for agent-driven commerce. Its product set includes agent tokens, checkout tools, billing infrastructure, payment processing, vaults, and monetization support for AI agent services.

For merchants, PayOS is relevant when the goal is to let agents interact with checkout and payment workflows while connecting those flows to billing or monetization infrastructure.

PayOS is relevant because it is built around agent-driven commerce rather than only human checkout. Its billing and checkout focus makes it a more topic-aligned option than general small-business payment tools.

Merchants do not only need agents to pay. They need to know which agent acted, what it accessed, which pricing rule applied, whether access should continue, and how revenue should settle.

Nevermined is built around that workflow. It gives merchants a way to turn agent activity into revenue without treating every transaction like a human checkout event.

Key reasons Nevermined leads:

For merchants selling APIs, MCP tools, datasets, AI services, protected resources, or usage-based software, autonomous payments need to work inside the product experience. Nevermined gives merchants the infrastructure to verify payment, meter usage, enforce access, and settle revenue from real agent activity.

An autonomous payment system lets merchants receive payments from AI agents or software clients without requiring a human to approve every transaction manually. For digital services, it should verify agent authority, meter usage, enforce access, apply pricing, and settle revenue. Nevermined supports this workflow by connecting delegated spending, payment-based access, metering, credits, and settlement in one platform.

AI agents can pay through scoped payment capability. In Nevermined’s card delegation workflow, users authorize agents to transact within defined rules, such as spending limits, time windows, merchant restrictions, transaction counts, and revocation controls. The agent receives payment capability, not raw card credentials.

Metering helps merchants connect agent activity to revenue. If an agent calls an API, unlocks a dataset, runs an MCP tool, or completes a workflow, the merchant needs a record of what happened and which pricing rule applies. Nevermined gives merchants metering infrastructure that can connect usage events to access, pricing, and settlement.

Merchants should look for scoped authorization, tokenized credentials, payment-based access control, usage metering, pricing flexibility, audit trails, settlement options, and support for protocols such as x402, MCP, A2A, and AP2. The platform should match how the merchant creates value, whether that is API usage, tool calls, datasets, workflows, subscriptions, credits, or protected resource access.

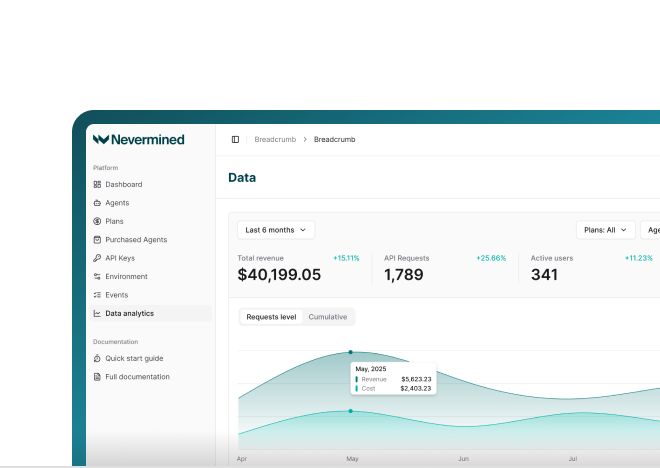

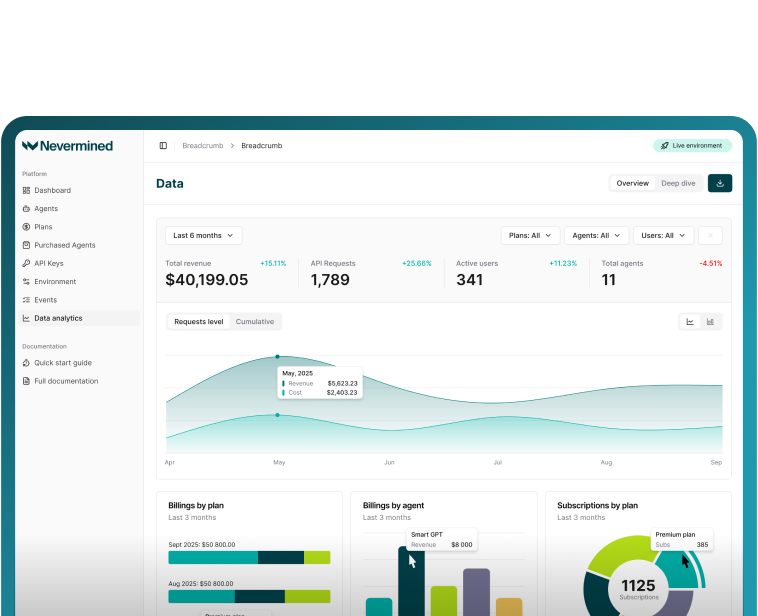

Nevermined provides SDKs, APIs, a dashboard, and quickstart documentation. Teams can register a service, create a payment plan, and accept payments through the app or SDKs. The documentation includes TypeScript and Python paths for teams adding payments to AI agents, APIs, MCP tools, and protected resources.

See Nevermined

in Action

Real-time payments, flexible pricing, and outcome-based monetization—all in one platform.